At first glance the job market in 2026: Trends and Predictions on the American labor market appears remarkably serene. With the national unemployment rate hovering steadily at 4.3%, many observers have mistaken this “low-hire, low-fire” environment for a return to pre-pandemic normalcy. But beneath this veneer of stability, the structural architecture of work is undergoing a fundamental unbundling. The traditional 40-hour workweek is no longer a monolith; it is a fracturing relic.We have reached a high-efficiency equilibrium where the old social contract—trading a single employer’s loyalty for lifelong security—has been torn apart. In its place, firms are surgically unbundling roles into automated tasks, gig-based hedges, and specialized modalities. This isn’t a “slow” market in the traditional sense; it is a strategic adaptation. To understand this new economy, we must look past the aggregate numbers and recognize that while the surface is calm, the tectonic plates of employment have shifted permanently.

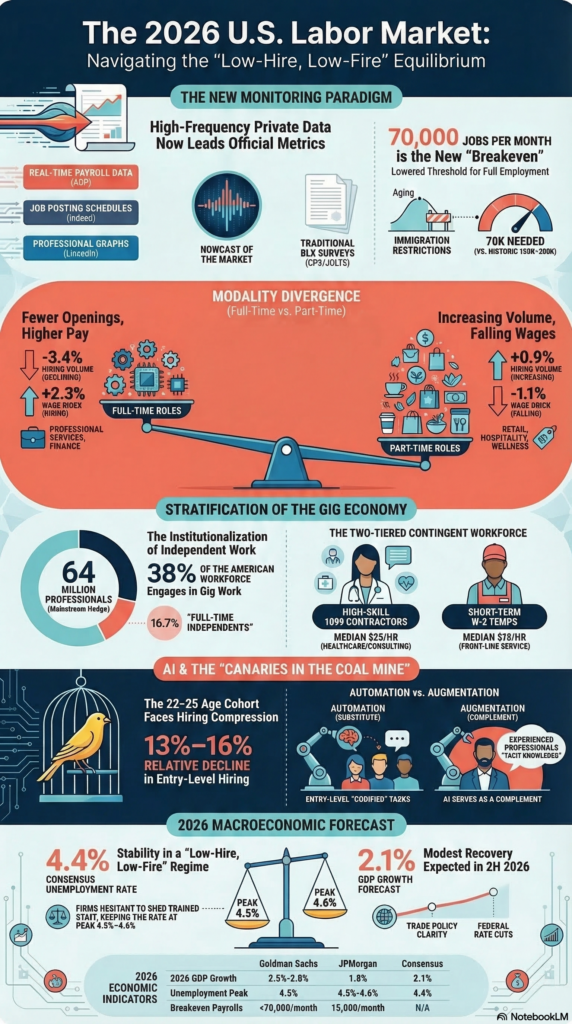

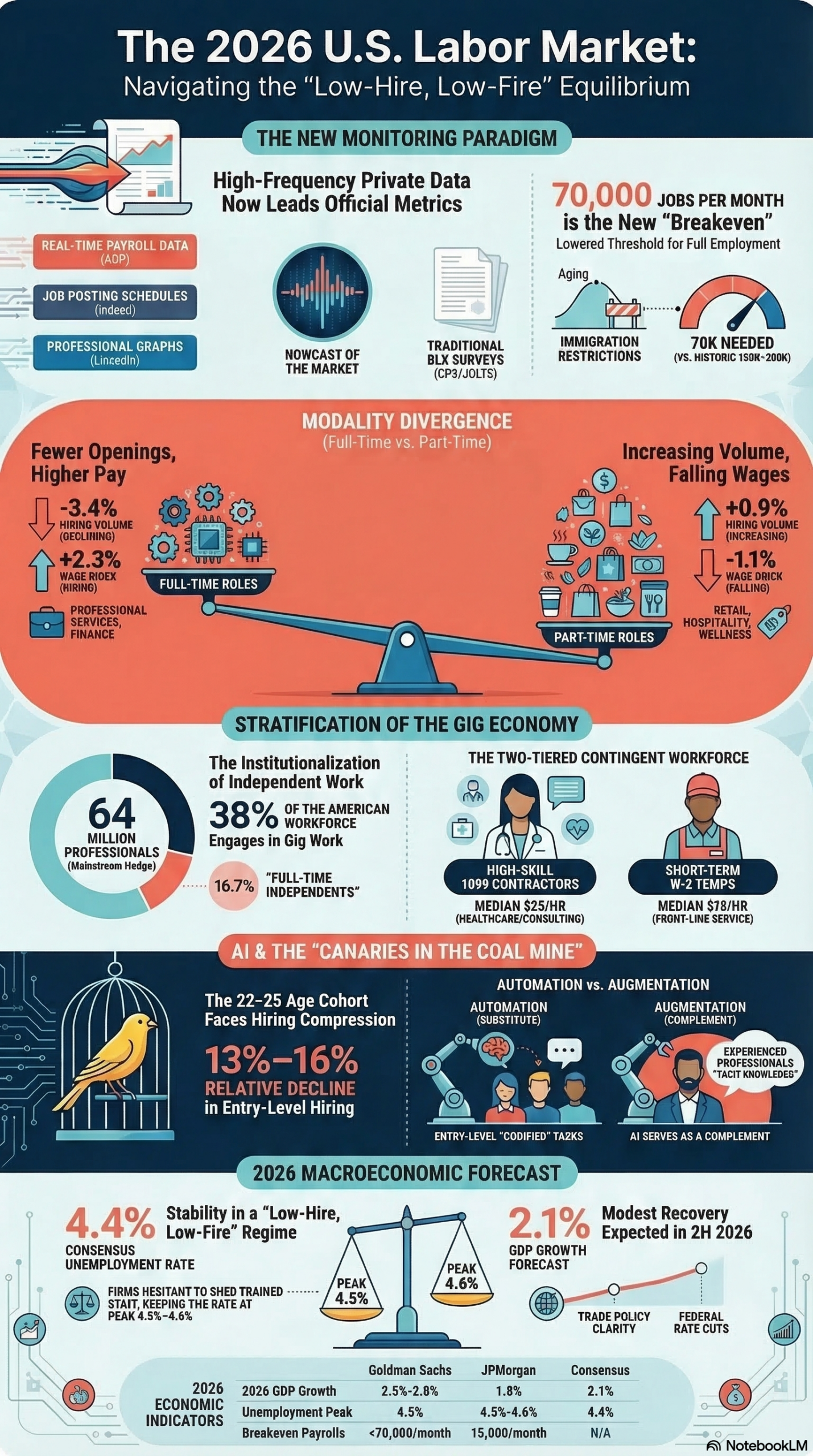

1. The 70,000 Rule: Redefining “Full Employment”

For decades, the “breakeven” job growth rate or the number of new roles required to keep unemployment steady—was anchored at roughly 200,000 per month. In the 2026 job market, that floor has dropped through the basement. A combination of the aging baby boom generation (subtracting 2.5 percentage points from labor participation) and tighter immigration flows has drastically lowered the bar for economic success.When the economy added 130,000 jobs in January 2026, headline-readers cried “slowdown.” Labor economists, however, saw a massive over-performance. Because the labor supply is growing so much more slowly, the economy can now maintain full employment with a fraction of the historical hiring volume.”Estimates for the new breakeven rate vary between institutions, but the consensus is clear: Goldman Sachs projects the economy needs fewer than 70,000 jobs per month to maintain stability, while JPMorgan suggests the floor may be as low as 15,000.”This lower bar means a “low-hire” environment is the new sign of a balanced market. Success is no longer measured by the quantity of new bodies in the room, but by the efficiency of the matches that remain.

2. The Great Swapping: The Bifurcation of Modality

Work is being unbundled from the traditional full-time schedule. Data from the Indeed Hiring Lab shows a stark “swapping” of employment types: since 2022, the share of job postings for specifically full-time roles has stagnated, while part-time postings have surged to 31.7% of all advertisements.Crucially, this isn’t just a shift in hours; it is a divergence in job quality. We are witnessing a compositional change where “full-time” is becoming a premium product. According to the Upjohn Institute’s New Hires Quality Index (NHQI), the few full-time roles being created are increasingly specialized, while the part-time surge is concentrated in lower-wage service tiers.

The Job Market: Employment Modality Comparison (2025–2026)

| Metric |

Full-Time Roles | Part-Time Roles |

| Hiring Volume Trend | -3.4% (Declining) |

+0.9% (Increasing) |

| Wage Index Change | +2.3% (Rising) |

-1.1% (Falling) |

| Sectoral Concentration | Professional Services, Finance | Retail, Hospitality, Wellness |

3. The AI “Canary”: Structural Ladder-Kicking

The most profound unbundling is occurring at the entry-level. While generative AI is often framed as a future threat, for workers aged 22–25, the disruption has already manifested as “structural ladder-kicking.” Research from the Stanford Digital Economy Lab, titled Canaries in the Coal Mine, shows a 13% decline in hiring for this cohort in AI-exposed roles like software development and clerical work.

The irony of 2026 is that AI is currently a boon for the “incumbents.” Morgan Stanley data shows that experienced professionals are using AI as an augmentative tool to save 10–15 hours per week, essentially unbundling themselves from the drudgery of administrative tasks. However, those very tasks were once the training ground for new graduates. By automating the bottom of the pyramid, firms are inadvertently destroying the entry-level ladder.

“The pace of this unbundling is breathtaking. Between 2023 and 2024, AI systems improved their performance on software engineering benchmarks from a mere 4.4% to a staggering 71.7%.”

4. Gig Work as the New Corporate Hedge

The most dramatic surge in the labor market is the institutionalization of the independent sector. By 2024, the number of “full-time independents” hit 27.7 million—a 104% increase since 2020. This shift represents a psychological unbundling of “security” from “the employer.” Workers no longer view a single salary as a safe harbor; they view it as a single point of failure.

However, the independent market is itself bifurcated by skill and pay. The “quality of life” gap between those with high-value technical skills and those in temporary labor is wider than ever.

The Independent Talent Divide:

- The 1099 Professional: Median pay for independent contractors stands at $25/hr, with nearly 7% earning over $100/hr. These are high-skilled advisors in finance and tech who use multiple income streams as a superior defense against layoffs.

- The Short-Term W-2: Median pay for temporary employees remains stagnant at $15/hr. These workers trade stability for flexibility but lack the “portfolio power” of the 1099 cohort.

- The Motivation Shift: 65–68% of independents now feel more secure than traditional employees, citing the ability to control their own “revenue stack” rather than relying on a corporate benefactor.

5. The Urban-Rural Reward Gap

The final unbundling is geographic. Technology was supposed to “flatten” the labor market, but in 2026, the economic rewards are more concentrated in metro hubs than ever. According to the Upjohn Institute, new hires in metropolitan areas have seen real wage growth of 5.4% over the last decade. In non-metro areas, inflation-adjusted earnings for new hires have remained essentially flat.

This stagnation is driven by the rural economy’s continued reliance on the “goods-producing sector,” which has been hit hardest by tariff-induced headwinds and trade policy volatility. While the “likelihood of getting hired” is down across the board, the payoff for landing a role in a tech-centric urban center is vastly superior to the returns found in the rural periphery.

——————————————————————————–

Conclusion: The Unbundled Future

The U.S. labor market of 2026 is not failing; it is rebalancing toward a high-frequency, skills-first reality. We anticipate a modest second-half rebound as the stimulative effects of the “One Big Beautiful Bill Act” (OBBBA) take hold and the Fed continues its cycle of rate cuts.

But let there be no mistake: the market we are returning to is structurally distinct. We face a growing risk of “jobless growth,” where firms leverage AI and flexible modalities to meet rising demand without ever expanding their permanent payrolls. In this unbundled world, the most successful participants will be those who stop looking for a “job” and start building a portfolio of skills and income streams that transcend traditional institutional boundaries. The 40-hour workweek may have been the king of the 20th century, but in 2026, the king is dead—long live the portfolio.

Key Takeaways

- The Job Market in 2026 reflects a shift toward low-hire environments, where fewer jobs are needed to maintain full employment.

- The 70,000 Rule suggests the economy only requires 70,000 jobs per month to stay stable, marking a significant change from historical norms.

- Work unbundling leads to a rise in part-time roles and specialization, making full-time jobs increasingly rare and valuable.

- AI disrupts entry-level roles, automating tasks that traditionally trained new graduates and creating a structural barrier.

- Gig work grows as a preferred employment model, with independents feeling more secure than traditional employees despite a widening pay gap.

Estimated reading time: 6 minutes